The Troubles of Addiction

The Troubles of Addiction

Financial markets have been addicted to overly accommodative monetary policy for years. Its removal is likely to cause significant withdrawal symptoms.

Quitting any addictive substance is hard. Whether it's caffeine, chocolate, or cigarettes, cutting it out of your life is likely to trigger withdrawal symptoms, including but not limited to profuse sweating, headaches, and irritability.

Financial markets have long been addicted to easy monetary policy. Years of rate cuts and asset purchases hooked investors on accommodative interest rates and large-scale central bank purchase programs. These measures generated a buzz in financial market returns while dampening volatility. However, central banks are now withdrawing this addictive medicine as they scale back bond buying and hike interest rates to combat inflation. Markets are already showing some side effects: higher volatility and greater dispersion. Investors need to learn how to manage these withdrawal symptoms properly, as they are unlikely to disappear anytime soon.

The Shakes Begin

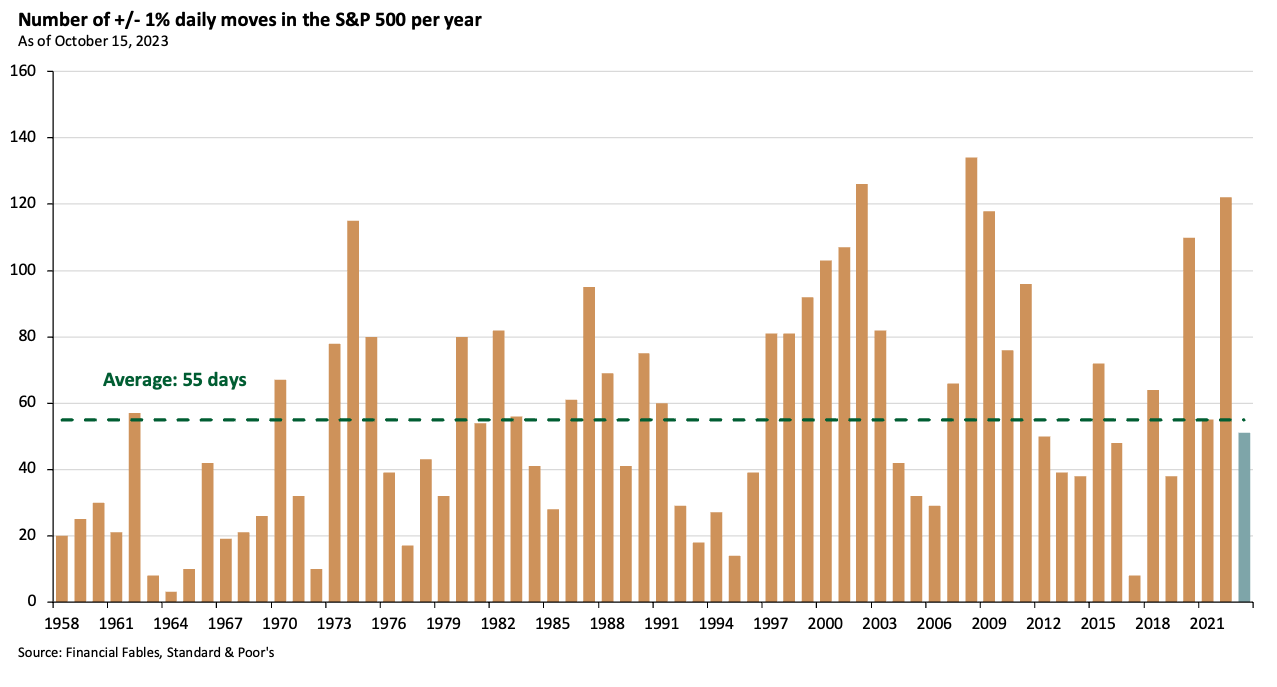

The return of financial market volatility is likely to be a consistent feature in a world with less quantitative easing (QE). There are various technical ways to measure volatility; however, I prefer a simple and relatable approach: the number of days the S&P 500 moves more than 1% in either direction. Although the 1% threshold is somewhat arbitrary, a move of this magnitude is widely considered meaningful in the US equity market on any given day.

Since 1958, the S&P 500 has experienced an average of 55 days a year where its price moves +/- 1%. However, the introduction of loose monetary policy altered this phenomenon. Since the Fed's introduction of open-ended asset purchases in 2012, the number of 1% days fell to an average of just 41 over the following five years. 2017 was a particularly extreme year, with only 8 days where the market shifted +/- 1%.

However, the onset of COVID and the subsequent return of inflation have changed this subdued dynamic. In 2020, there was particularly high volatility, with 110 days of +/- 1% movements. Then, in 2022, movements in global interest rates resulted in the index registering its third-highest total in history, with 122 volatile days. Year to date, the S&P 500 has experienced 51 days, a pace that, if continued, would take the market well over the long-term annual average. In short, the withdrawal of easy monetary policy is already making itself felt in equity markets. Investors need to deal with these troubling withdrawal effects, as it is unlikely central bankers will reintroduce addictively loose monetary policy anytime soon.

Withdrawal Symptoms & Side-effects

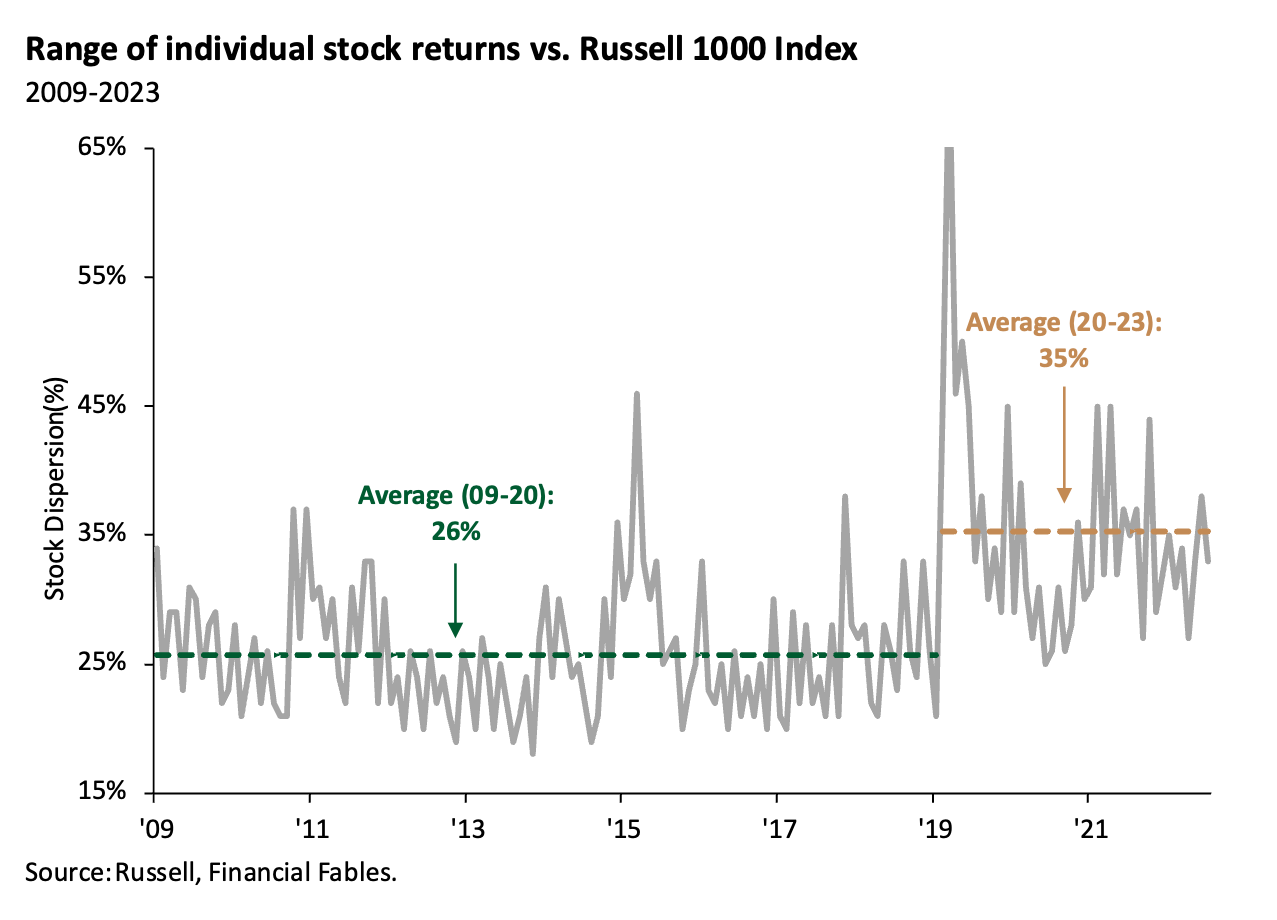

One of the many challenges with addictive substances is that they numb you to the outside world and can lull you into a disorienting sense of complacency. It is quite a jolt when these substances are removed. The last decade of excessive central bank easing has suppressed sector and security selection, hampering effective security analysis. Extensive quantitative easing helped lift all financial assets, with valuations being dictated more by top-down monetary policy decisions than by effective bottom-up security analysis. When the price of every security rises and falls in unison, there is little need to distinguish between good and bad companies. It is hardly a great environment for security selection.

However, the rise in interest rates enforces a degree of discipline on market participants and forces them to take a more discerning approach when judging viable investments. Against this backdrop, sector and security dispersion are likely to rise as investors begin to adjust to a world that is no longer awash with dangerously addictive uber-loose monetary policy. As we show in the chart below, dispersion within equity markets has already begun to rise, and we seem to have embarked on a new dispersion regime. A financial market with wider dispersion should make it easier for active managers to showcase their stock-picking skills and outperform their passive, benchmark-tracking competitors.

The detox from the era of uber-loose monetary policy is likely going to be a painful experience characterized by higher levels of volatility. While active management is likely to make a return, we may also witness the return of an old, somewhat forgotten friend: hedge funds.

Return of the Hedge Fund?

One of the biggest losers in the era of ultra-low interest rates has been hedge fund strategies. Between 2013 and 2022, the average annual return for hedge funds has been 4.9%, according to HFRI composite. In comparison, global equity markets have returned 8.5% per year over the same time period. So, it’s not that hedge funds have performed poorly; it’s just that in an era of smooth sailing, investors have not needed them.

Where hedge funds begin to demonstrate their value is when we sail into choppier waters. The relative calmness of financial markets over the last decade has meant it’s been rare to see elevated turbulence in financial markets. Hedge funds need some turmoil as it generates opportunities for managers to exploit market inefficiencies, which are often most acute when investors are panicking, in order to deliver alpha to clients.

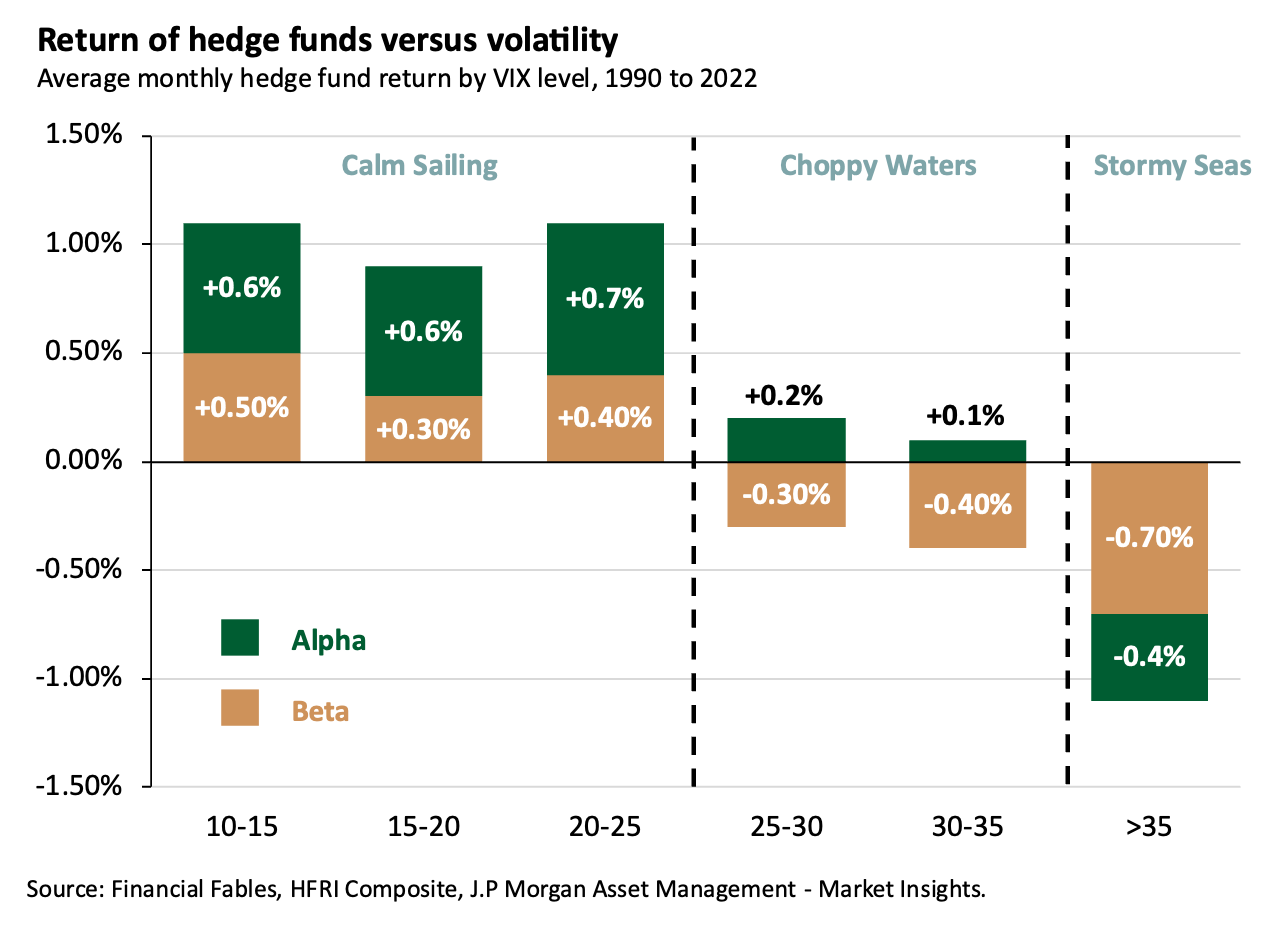

To put this into practice, the chart below shows the market return (beta) and the return generated above the market (alpha) by hedge funds in different market environments (measured by the VIX index). When the waters are calm, it is plain sailing as both the market and the alpha from hedge funds remain positive. This is the environment we have been in for much of the last decade.

However, when the VIX begins to rise to between 25 and 35, we get into choppier waters, and economic conditions begin to get stressed. In these conditions, the market return quickly turns negative; however, this is where hedge funds demonstrate their value as they continue to generate positive alpha. It’s only in the stormiest of seas (+35 on the VIX) that the dynamic finally breaks, and both alpha and beta turn negative. The environment we are entering into is unlikely to be seen as a crisis, but elevated interest rates could see us stay in these choppy waters for a while, a point where hedge funds play a valuable role in investors’ portfolios.

However, the term ‘hedge funds’ is a large umbrella that covers a wide range of different strategies. Investors should get picky about which areas they’d like to focus on. Against the backdrop of elevated and prolonged volatility, Global Macro hedge funds typically exhibit higher returns. In addition, at this stage in the cycle, distressed credit may be worth looking into as well. If defaults move higher, distressed credit can exploit the situation and manage to pick up a number of interesting opportunities at bargain prices.

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as financial, investment, or professional advice. The content is not intended as a solicitation, recommendation, endorsement, or offer to buy or sell any securities or financial instruments. Any reliance you place on such information is strictly at your own risk. Always consult with a qualified financial advisor or professional before making any investment decisions. The author and the website assume no responsibility for any losses or damages that may result from the use of or reliance upon the information provided in this blog post.