The Cautionary Tale of the Whale and the Pond

Financial market liquidity is poorly understood and rarely considered. Investors should be wary of the problems it can cause.

For whales to live they need plenty of deep, open water in which to frolic and hunt. Restricting the movements of these beautiful behemoths by raising them in captivity does not often end well for the poor whale. The risk posed by shallow waters is also true with regards to liquidity in financial markets and can become a particularly acute issue during periods of market stress.

Market liquidity is often a difficult topic to define, it’s a complex and transient issue. However, for the purposes of this post let’s use the most intuitive definition which is ‘the ability of investors to efficiently buy or sell an asset without disrupting market pricing’. The ability to easily transact in the market place, particularly in certain areas of the bond market, has become an increasing issue over the last few years.

Who drained the pond?

Today’s proverbial pond used to look much more like an open ocean prior to the Global Financial Crisis. Pre-2008 financial institutions had significant discretion as to how to manage the risk on their balance sheet. Banks were allowed to engage in wide-spread proprietary (prop) trading. Prop trading was a lucrative activity whereby a bank used its own capital (rather than its clients) to trade in financial markets. While this activity may seem innocent on the surface it came into the lime light in the aftermath of the financial crisis as regulators questioned whether it created direct conflicts of interest between banks and their clients. New regulation in the form of the Volker Rule dramatically scaled back the ability of banks to engage in prop trading, essentially restricting them to market-making and client servicing actions. Regardless of the desire behind the regulation, its effects had a profound impacted on the shape of fixed income markets, particularly in the corporate debt markets. As shown in the below chart ‘dealer inventory’ which reflects the amount of bonds traders have on their own balance sheets, collapsed following the financial crisis.

Today, dealer inventories are a small fraction of where they were prior to 2008, meanwhile the corporate bond market itself is now 3.5x bigger than it was prior to the Global Financial Crisis. To return to our Whale and the Pond analogy – not only is the pond significantly shallower but the whale has also grown… a lot!

How big of an issue is it?

Illiquidity issues are not a constant feature in the day-to-day market trading. This lack of liquidity is best viewed as a hidden risk, only rearing its head during a crisis when a large number of investors are all attempting to quickly move in the same direction at the same time. In effect, illiquidity is not the trigger of a market sell-off but its presence tends to enhance extreme selling pressures and intensify the size of the drawdown. A good example of this in action was seen in September 2022, where financial markets were spooked by a number of unorthodox policy announcements by Liz Truss and her Chancellor, Kwasi Kwarteng. The interest rate on UK 10-year government debt rose from 2.81% at the start of September to 4.51% by the end of the month, its highest level since 2008. As bond yields rose, UK pension funds were forced into action to re-balance their portfolios and meet collateral calls. However, as these giant institutions tried to trade they found that market liquidity had dried up; they were trying to sell but there was nobody willing to buy. If this happens, investors are forced to slash prices in order to tempt in a buyer but this compounds the market sell-off even further. In the end, the liquidity situation became so dire that the Bank of England had to step in to prop up the markets and help pension funds navigate this challenging period. Simply put, it is not possible for whales to turn quickly in ponds.

How have investors responded to the risk?

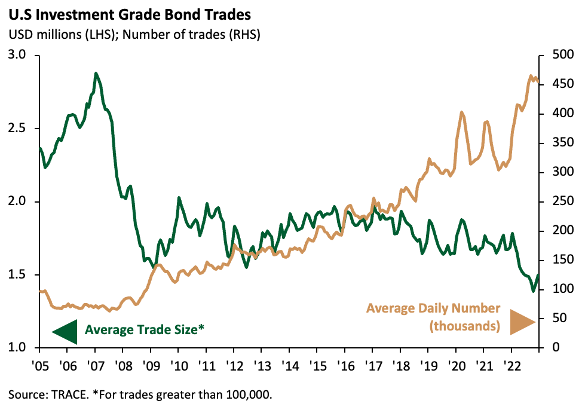

Navigating these shallow markets is difficult for investors, particularly if they are trying to execute at size. One option that has been deployed, is for market participants to try and ‘slice and dice’ their trading activity. In the second chart, investors have cut down on their average trading size to smaller and smaller levels. Meanwhile the number of trades in the corporate bond market has increased 5-fold since the Financial Crisis.

But attempting to be small and nimble comes at a cost. Bigger bulkier trades often come with a discount however, this ‘slice and dice’ strategy can force up transaction costs. Without the economies of scale derived by bigger trade, very large investment funds can have a hard time building or unwinding a particular investment position without incurring significant trading expenses. Stated simply, a lack of liquidity is making it more dangerous and expensive to be a big fish in an increasingly small pond.

What should investors do about it?

Managing illiquidity in the fixed income markets is not a simple task. The topic often has a transient effect on markets before receding but can be particularly painful for investors during those periods where market functionality comes to a sudden stop. One beneficial approach is to discuss the options with investors through the lens of ‘defensive’ and ‘offensive’ approaches to managing periods of illiquidity.

Here are three approaches I would think about:

1. Keep calm and do nothing

One defensive option is to quite simply do-nothing during periods of illiquidity. By avoiding trading during periods of significant market dislocations investors don’t expose themselves to the painful transaction costs and significant mark down in prices. By keeping calm and carrying on, investor’s portfolio will experience a drawdown as they mark prices to market which will stay in their historical track record over time but ultimately is one approach for overcoming this challenge. Therefore, for retail investors taking a passive, benchmark-aware approach to investing is one way to persevere with this issue. Similarly, for large institutional clients they can implement a ‘buy-and-hold’ approach to bond investing whereby they are indifferent to price fluctuations or market illiquidity as long as the borrower repays the bond at maturity. The flaw to this approach is when an investor is forced to come to markets, perhaps there is a liquidity event, a collateral call or looming corporate defaults that an investor wants to avoid. In this instance it is forced to accept a sharp write-down in the value of their holdings which can be painful during liquidity crunches.

2. Focus on the smaller fish

Returning to our ‘Whale & the Pond’ story, one option is that investors could look to avoid the whales entirely, focusing instead on the smaller fish that are much more appropriately sized for the shallow waters. Some of the largest bond funds are now over $100 billion in size. While markets can usually absorb their moves without too many issues, it is difficult for these titans to quickly switch their sizable positions without causing waves that disrupt the market place. In comparison, smaller bond funds cause less of a splash and should be able to swiftly reposition in response to any economic or financial news without incurring sizable transaction costs.

3. From prey to predator

The previous two strategies were primarily defensive, essentially treating market illiquidity as something to run and hide from. A more offensive option is to take on the role of liquidity provider to the market place but only on terms that are beneficial to you. This is role that is partly played by unconstrained, absolute return fixed income funds that look to deploy cash and jump into markets when others are selling. This contrarian approach may not be appropriate for more risk averse investors but it involves offering to buy assets at often heavily discounted prices and then wait for markets to stabilize and asset prices return to something resembling fair value.

If you enjoyed this piece and want to hear more financial fables please consider subscribing to Financial Fables.

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as financial, investment, or professional advice. The content is not intended as a solicitation, recommendation, endorsement, or offer to buy or sell any securities or financial instruments. Any reliance you place on such information is strictly at your own risk. Always consult with a qualified financial advisor or professional before making any investment decisions. The author and the website assume no responsibility for any losses or damages that may result from the use of or reliance upon the information provided in this blog post.