Plug-holes and debt spirals

The U.S debt dynamics are being sucked towards a dangerous vortex

As any parent will testify, bath time is often a chaotic experience. As one parent tries to keep as much water in the tub as possible, the other is often trying to get the rest of the house in some semblance of order. However, in the madness of our bedtime routine, there is usually one moment of silence, which is when the plug is pulled from the bath. I am not quite sure why the swirling water around the plug hole catches our son’s attention, but it does provide us with a moment of peace and quiet. As we silently sit together and watch this vortex, my (sad) economics mind can’t help but think that this watery downward spiral looks a lot like the current US debt dynamics, which are also seemingly circling the plug hole!

A dangerous vortex

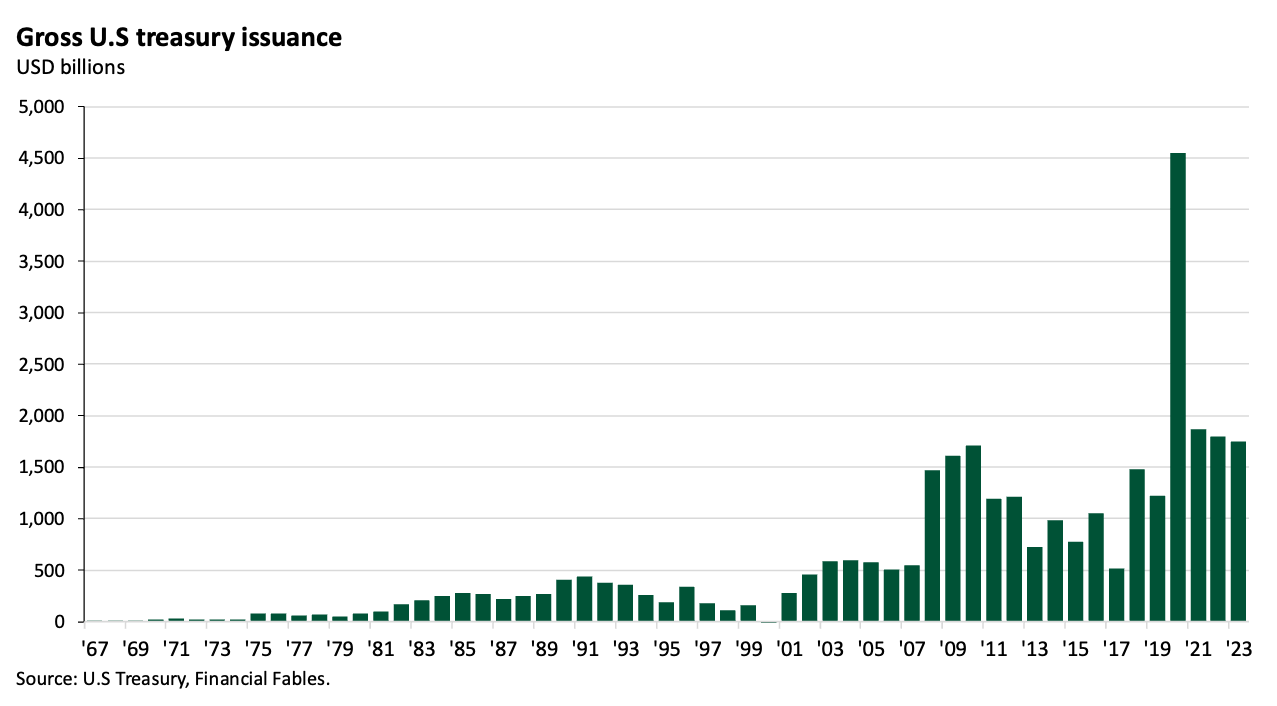

Since the onset of COVID-19, US debt issuance has been going at an extraordinary pace. Over the last four years, gross debt issuance has exceeded $10 trillion. Unfortunately, this is unlikely to improve any time soon. Goldman Sachs estimate that net debt issuance will exceed a record $1.4 trillion this year, well above last years net issuance figure of $391 billion.

With a deluge of supply set to hit the market this year, economists are beginning to be concerned that the US is entering a debt spiral, whereby large amounts of debt issuance beget even more debt issuance.

The issue with debt spirals is that once they begin, they become hard to stop. Increased debt issuance drives up bond yields as fiscal security begins to be jeopardized. An increased cost of borrowing sees more money diverted to servicing the growing debt burden, which further widens the budget deficit, causing even more debt to be issued, and around and around we go.

Breaking out of a debt spiral is a tricky business and requires either significant growth and/or strong consensus across the political spectrum to tackle the issue. If you’d like to hear me chatting about debt spirals (and how to get out of them), check out the video below:

However, with the debt burden mounting, investors are rightly pondering who is going to buy all this debt? For much of the last decade, quantitative easing (QE) programs meant that the U.S Federal Reserve were able to hoover up much of the government bond issuance. At its peak, the Fed were the single biggest holder of U.S public debt, owning over 20% of the U.S debt burden. But today the Fed have switched their QE program into reverse and are effectively conducting quantitative tightening (QT) and have shrunk their balance sheet by approximately $1.3 trillion, reducing their proportion of US debt ownership. With the Fed no longer buying up bonds, who is buying all this newly issued US debt?

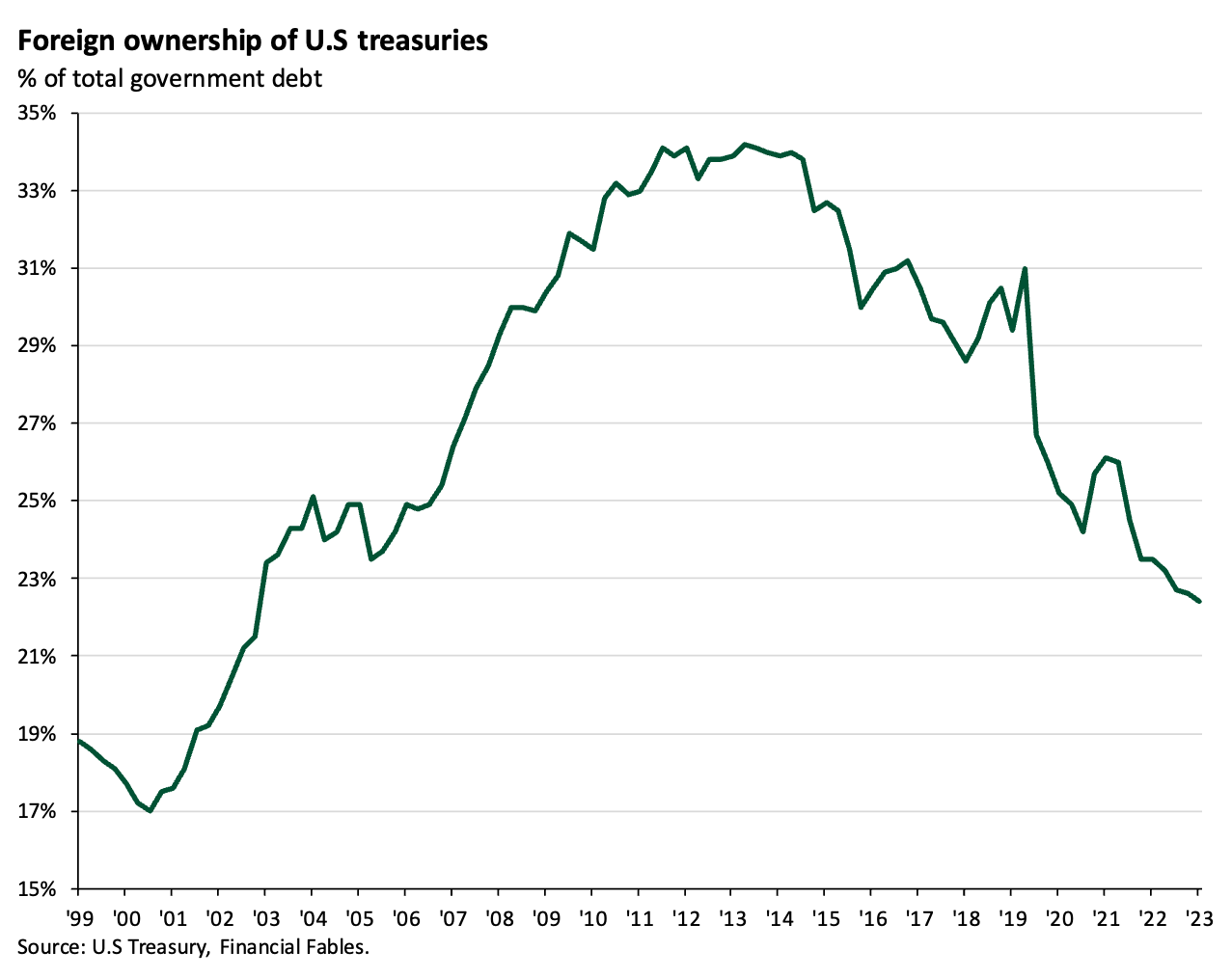

Dwindling Foreign Ownership

For years, the U.S. has been able to benefit from its position as the world’s reserve currency by issuing large amounts of debt to foreign investors. At its peak, the insatiable appetite for U.S. government debt saw foreigners owning nearly 35% of all debt issuance. However, since then, that figure has slipped

.Some bond watchers note that the decline in foreign ownership began when President Trump came into power and cited this fall as a sign that foreign investors were losing faith in the stability of the US given the election of an unorthodox politician. However, a large proportion of the decline following the election was driven by a fall in demand from official Chinese investors who have sought to recycle the funds back into their domestic markets.

While Chinese investors sought to withdraw from US debt markets, there is one group of bondholders who still hold onto their U.S. government debt: the Japanese. Japanese investors hold an estimated 17% of U.S. Treasury debt, the single biggest ownership group behind the U.S. Federal Reserve.

However, even amongst Japanese investors, the challenges are beginning to mount as currency hedging costs are making it increasingly expensive for Japanese investors to access US debt markets. Hedging costs are a function of the interest rate difference between two countries. Considering that the U.S. Fed has hiked rates significantly while the Japanese have not moved an inch, the interest rate difference between the two countries is now particularly large. The effective cost for a Japanese investor to hedge their currency exposure for one year was 15 basis points. As of February 24, 2024, it was the equivalent of 555 basis points. This means that a Japanese investor holding a U.S. 10-year bond, yielding 4.3% and then opting to hedge the currency exposure for a year, is effectively guaranteeing themselves a loss.

Theoretically, Japanese investors could just opt to leave the currency position unhedged. However, this could represent a significant increase in the risk of managing their portfolios as currency markets can be highly volatile. Instead, it seems probable that Japanese investors will look to gradually rotate portfolios away from the US debt markets until currency hedging costs return to more reasonable levels.

Any other buyers?

With both the central bank and foreign investors stepping back from U.S treasury ownership the question as to who is going to own the spiraling amounts of US debt remains unanswered. Some of this supply will be covered by Money Market Funds (MMFs) and additional savings from households however, there is a more concerning source of demand from leveraged funds.

These leveraged funds have been exploiting arbitrage positions between cash bonds and futures. Usually, this difference is tiny, but if you leverage up your position and move huge volumes this trade can pay-off. The issue is that the Bank for International Settlements has warned that this speculative activity in treasuries markets "is a financial vulnerability", and a Fed paper in 2023 said it warrants "diligent monitoring".

Theoretically, these leveraged positions are not necessarily an issue for market stability, as long as market turbulence remains relatively calm however, if volatility starts to pick-up the huge amount of speculative activity in bond markets could trigger more volatility and result in the debt spiraling speeding up even more. In short, US debt dynamics continue to circle a dangerous looking plug hole.

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as financial, investment, or professional advice. The content is not intended as a solicitation, recommendation, endorsement, or offer to buy or sell any securities or financial instruments. Any reliance you place on such information is strictly at your own risk. Always consult with a qualified financial advisor or professional before making any investment decisions. The author and the website assume no responsibility for any losses or damages that may result from the use of or reliance upon the information provided in this blog post.