Between Scylla and Charbdis

Central bankers are hell-bent on getting inflation under control, even if that means risking a recession

In Greek mythology, the hero Odysseus had to navigate a perilous stretch of water while returning home. A narrow strait presented two hazards: Scylla and Charybdis. Scylla was a many-headed sea serpent that attempted to pluck sailors from ships as they passed. Meanwhile, Charybdis was commonly depicted as a whirlpool or a subaquatic monster lurking beneath the surface, attempting to suck the entire ship into the murky depths. Sailors approaching this perilous passage were essentially faced with an impossible choice: sail past Scylla and risk losing a number of the crew to the ferocious demon, or chance it with Charybdis and hope the entire ship doesn’t get drawn down into the abyss.

Central bankers are faced with the same epic challenge in their journey to navigate the economic ship through this tumultuous storm. Their choice is a daunting one: navigate close to Scylla and allow inflation to run hot. The many-headed inflationary hydra would almost certainly kill off a number of businesses and cause widespread damage, but the economic ship would probably stay afloat. Alternatively, they could strike a course close to Charybdis, getting inflation down quickly through significant monetary policy tightening, and just hope that they are nimble enough to be able to escape a recession that sinks the boat.

Steering sharply from Scylla

At Jackson Hole this week, it has become crystal clear which monster they would rather face. In his speech, Fed Chair Jay Powell noted that inflation had moderated but it was still too high and that policymakers were “prepared to move rates further” in order to properly control inflation. The takeaway for investors is that central bankers are willing to risk a full-blown recession in order to regain control over pricing pressures.

Indeed, the current inflation figures remain above target in many developed countries but their trajectory is unmistakably downward. In the US, almost all inflation components (with the exception of shelter prices) have reverted to more reasonable levels after reaching their peak in June 2022. Even the UK, the clear economic laggard, is finally witnessing a downturn in inflation. The chart displays the UK producer price index (advanced by six months) versus the UK CPI. It's noteworthy that the input prices paid by industries and services tend to provide a reasonable indication of the direction of consumer prices and currently suggests that inflation will moderate back to the Bank of England’s 2% target by the end of 2023.

However, despite this moderation in pricing pressure, policymakers are likely to persist with pushing through rate hikes, thereby increasing the risk of a recession. In reality, this chosen path should not be much of a surprise. The current cohort of central bankers are students of the inflationary turmoil of the 1970s and are great admirers of Paul Volcker, the head of the Fed in the 1980s, whose tough inflationary policies are widely credited with bringing rampant prices under control. Such a mindset implies that central bankers are unwilling to tolerate any inflation exceeding the target, and they will aim to quickly quell it, even if it entails the risk of being drawn into a recessionary vortex.

A Pretty Bleak Track Record

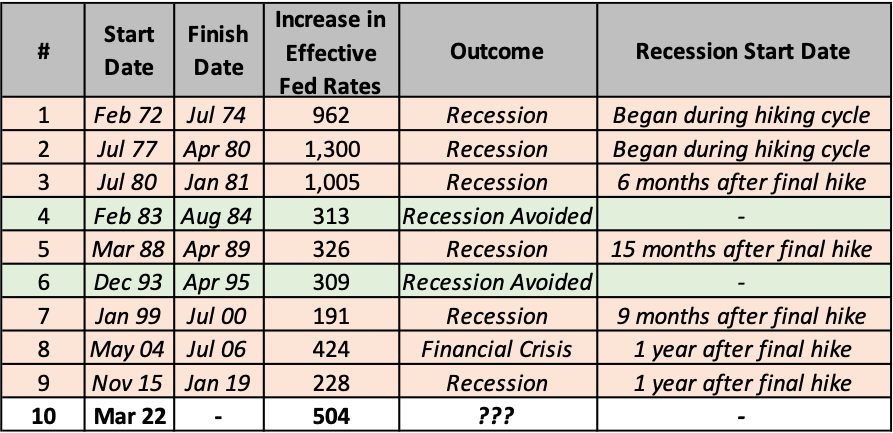

Navigating this hazardous body of water is a formidable task, requiring experienced sailors to position the sails perfectly so that the ship avoids elevated inflation without inadvertently causing a recession. However, that is easier said than done. The renowned economist, Milton Friedman, often discussed the 'long and variable lags' between monetary policy decisions and their impact on the real economy, which can range from as little as six months to as much as two years. These lagged effects likely explain why central bankers have such a dismal track record when it comes to successfully steering the ship through this tumultuous passage.

The table breaks down each of the nine Fed rate-hiking cycles that have occurred over the last 50 years, along with the ongoing tightening cycle that began in March 2022. Seven of the last nine rate-hiking cycles have led to a recession within 15 months of the final rate hike. On only two occasions has the Fed managed to slip quietly past the monsters without sinking the ship.

More sympathetic observers of central banks than myself might argue that in a number of instances (e.g., 1989 or 2019), the Fed was unlucky and that their plans were disrupted due to factors beyond their control, such as Iraq's invasion of Kuwait (1990) or COVID-19 (2020). Regardless of whether the Fed is to blame or not, this voyage seems to end in disaster many more times than it ends in success.

Are there any lessons that can be learned from these successful voyages that could increase the chances of success today? In the first of these instances, the tightening cycle of 1983-84, the economy was emerging from a double-dip recession. The Fed's objective was to normalize rates following an unsuccessful experiment with targeting the money supply, and inflation was stable. In short, it was a considerably less challenging journey than the ongoing rate-hiking cycle and was accomplished without the inflationary headwind.

The Fed's rate-hiking cycle in the mid-1990s is often cited as the perfect example of a successful tightening cycle, which solidified Alan Greenspan as a central banking legend. Policymakers were able to raise rates by over 300 basis points while unemployment actually decreased during this period. However, this cycle differs from the current one in that the Fed was not deliberately attempting to suppress inflation, with the Consumer Price Index (CPI) remaining around 3% throughout much of the tightening program and its immediate aftermath.

Can this time be different?

The task at hand is momentous, and it seems highly unlikely that the Fed can bring down inflation without causing an economic downturn. Even Fed officials themselves are skeptical. In a paper earlier this year, former Fed Vice Chair Alan Blinder, who presided over the successful rate-hiking cycle in 1994-95, highlights that it is "difficult, maybe impossible" for policymakers to accurately adjust monetary policy in real time. As Blinder confesses, much of the Fed's track record is dictated more by luck than skillful monetary policy.

The only successful voyages have been those where the Fed was not attempting to squeeze inflation out of the system. Investor skepticism can only be further compounded when considering how aggressive the current rate-hiking cycle has been compared to historical instances. The Fed has increased the Fed Fund rate by nearly 200 basis points beyond their two "successful" rate-hiking cycles. To exacerbate matters, the indebtedness of governments, corporations, and households means that each incremental rate hike inflicts significantly more pain on the real economy, as the burdensome debt amplifies its impact on each of the key economic actors. On balance, it therefore appears likely that the economic ship will eventually become ensnared in the recessionary vortex, despite the recent robustness of economic data.

The dangers of Charybdis

The tale of Scylla and Charybdis is believed to be the etymological origin of the term 'stuck between a rock and a hard place,' and that is precisely where central bankers find themselves. Neither path was appealing, and both carried their risks. However, in their attempts to aggressively steer the ship away from the inflationary monster, they have almost certainly set the economy on a course towards a recession in the near future.

At this point, it is difficult to accurately assess the nature of the impending recession; nevertheless, it is crucial for investors to recognize that it is unlikely to resemble the recent crises they have witnessed. One significant difference will be the monetary policy response. During COVID-19, the urgency of the pandemic and subsequent lockdowns prompted many developed and emerging central banks to engage in large-scale asset purchases. As the chart depicts, central banks were conducting purchases of up to 33% of their domestic GDP to support the economy and financial markets. Such extensive stimulus programs likely contributed to the inflationary challenges faced worldwide today, and central bank officials are highly unlikely to replicate their past actions due to the fear of triggering further inflation.

An inflation-induced recession also limits the ability of fiscal policymakers to respond adequately. In the aftermath of COVID-19, fiscal policymakers injected an estimated $10 trillion into the global economy, cushioning the impact of the pandemic on financial markets. However, with the wounds of inflation still fresh, it appears unlikely that fiscal policymakers will want to exacerbate the inflationary situation, thereby holding them back from implementing widespread spending programs.

With both monetary and fiscal policymakers effectively constrained, financial markets will be left to fend for themselves.

Corporate Downgrades: During the pandemic, corporations were shielded from the fallout by generous policymakers. In the US Investment Grade market, as little as 3% of the index was downgraded to high yield in 2020. In the next downturn, without the support of policymakers, that figure is likely to be higher, with estimates suggesting around 5% of the index could potentially be downgraded to junk.

Elevated Defaults: Throughout COVID-19, US high yield defaults reached 6%. While the high yield market has done its best to extend the duration of its borrowing, elevated defaults are still anticipated. Defaults have already been increasing and currently stand at around 2.7% as of the end of July. The substantial concentration of loss-making corporations could also contribute to heightened defaults, as higher interest rates push some of these companies into default, a risk discussed in a previous blog post.

Greater Dispersion: For much of the past decade, abundant monetary and fiscal policies created an environment in which investors had little need to differentiate between high and low-quality investments. During the next recession, the "policymakers' safety net" is unlikely to be as effective (or if it is, it will have a much higher threshold), leaving investors to manage the ensuing volatility on their own. In such a market, a more active approach to investment management is likely to yield greater value, given the widening dispersion between securities.

In the end, following advice from a wise mystic, Odysseus chooses to move past Scylla rather than risk complete ruin with Charybdis. Central bankers seem set to take a different course than the Greek hero and investors should likely brace for the potential economic turmoil that follows. As the pull of the recessionary whirlpool begins to influence financial markets investors should brace for the abyss.

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as financial, investment, or professional advice. The content is not intended as a solicitation, recommendation, endorsement, or offer to buy or sell any securities or financial instruments. Any reliance you place on such information is strictly at your own risk. Always consult with a qualified financial advisor or professional before making any investment decisions. The author and the website assume no responsibility for any losses or damages that may result from the use of or reliance upon the information provided in this blog post.